Iron ore’s most volatile week: How we got here and what comes next

Peter Hannah, 18 May 2021

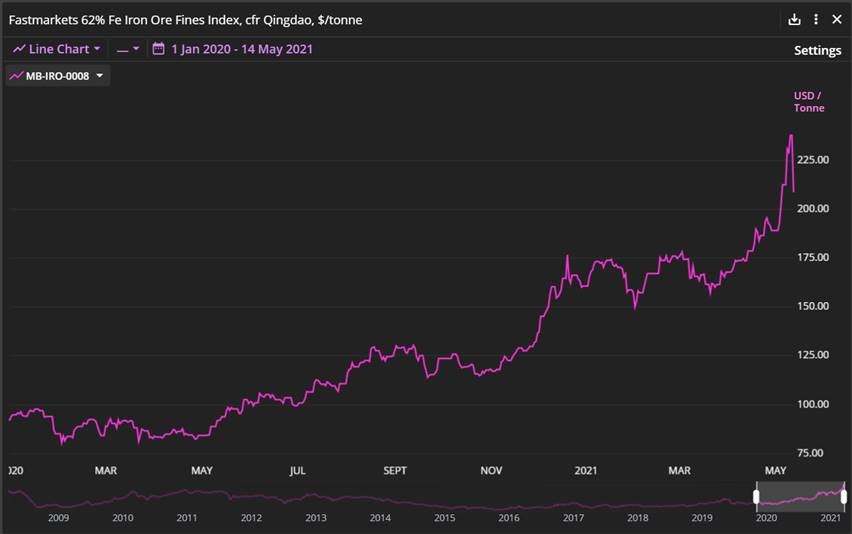

How did we get here? Of course, steel demand and iron ore supply do not change by multiple percentages over these daily timeframes. Mature markets trade as much on expectation as on current fundamentals, and changes in sentiment triggered by news and gossip can drive jarring session-to-session swings. However, panning out to a noise-reducing resolution, the explanations for iron ore’s current high price levels are very apparent.

How did we get here? Of course, steel demand and iron ore supply do not change by multiple percentages over these daily timeframes. Mature markets trade as much on expectation as on current fundamentals, and changes in sentiment triggered by news and gossip can drive jarring session-to-session swings. However, panning out to a noise-reducing resolution, the explanations for iron ore’s current high price levels are very apparent.

Regular attendees to industry conferences in recent years will have repeatedly heard the major iron ore producers laying out supply plans based on anticipations of Chinese crude steel production reaching the mythical 1-billion-tonne-per-year mark by 2025 at the earliest. Not only was that level exceeded a full five years sooner in 2020, but various production issues meant that iron ore supply also undershot projections.

Following its first economic contraction in decades in the first quarter of 2020 due to the coronavirus, Beijing responded with powerful stimulus measures that saw steel demand from the construction, infrastructure and consumer goods sectors hit previously unexpected levels. Despite China’s mills producing at record rates, steel prices began climbing from around the third quarter. By May 2021, domestic prices for billet, rebar and hot-rolled coil were all posting record highs, while steelmakers were enjoying their greatest profit margins since the supply-side reform peaks of 2018.